The resource buildout of the western grid used to support the limited markets scenario pricing and analyses incorporates many of the common assumptions that are used throughout the scenario work but removes the planning reserve margins for other planning areas throughout the western grid that are assumed throughout the other scenarios and the baseline. Removing the planning reserve margin is a proxy for other regions leaning heavily on west-wide diversity without explicitly building to a surplus to account for different regional risks[1].

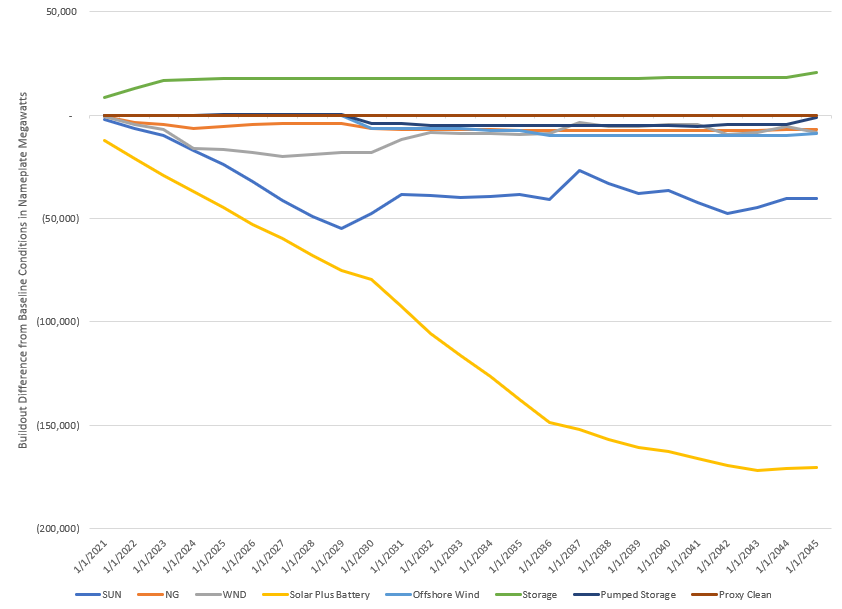

The associated buildout is significantly smaller than the baseline. Builds of all resources except storage are lower than the baseline. This study does still build a fair amount of zero or lower emissions resources early but primarily because they have lower production and fixed costs.

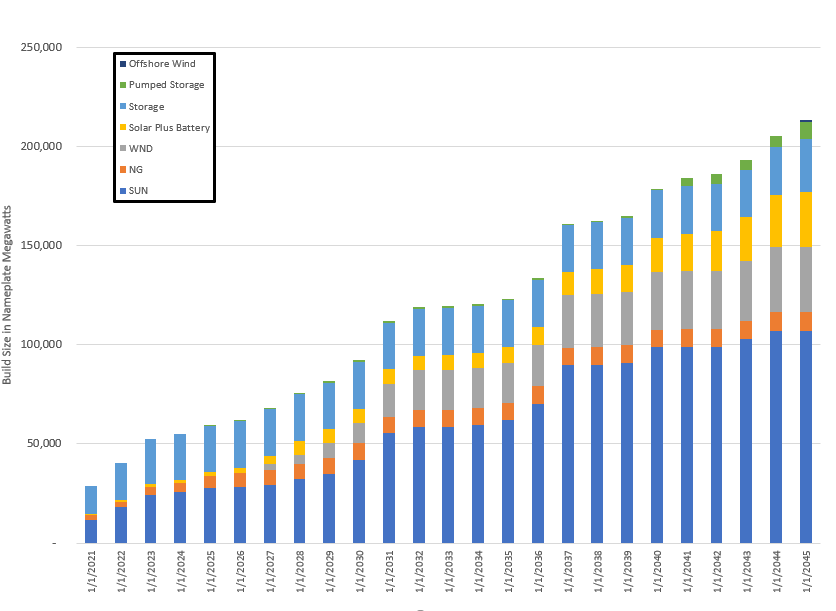

Limited Markets buildout

The buildout in the WECC-wide emissions pricing study included just under 185 gigawatts of nameplate build by 2041 as seen in the figure above. More than 63% of the new resource buildout was either stand-alone solar or solar plus battery hybrid resources, and over 79% of the buildout was solar or wind. Like in the baseline, significant amount of the renewable buildout appears to be to attempt to meet the policies enacted by states or municipal governments, and/or goals by utilities.

As can be seen below, significantly less stand-alone solar, hybrid solar plus storage and wind is built throughout the study. This seems to imply that under half of the renewable resources are being built due to clean and renewable policies, or economics, when comparing results to the baseline and no gas build limit buildouts[2].

Build Comparison to Baseline

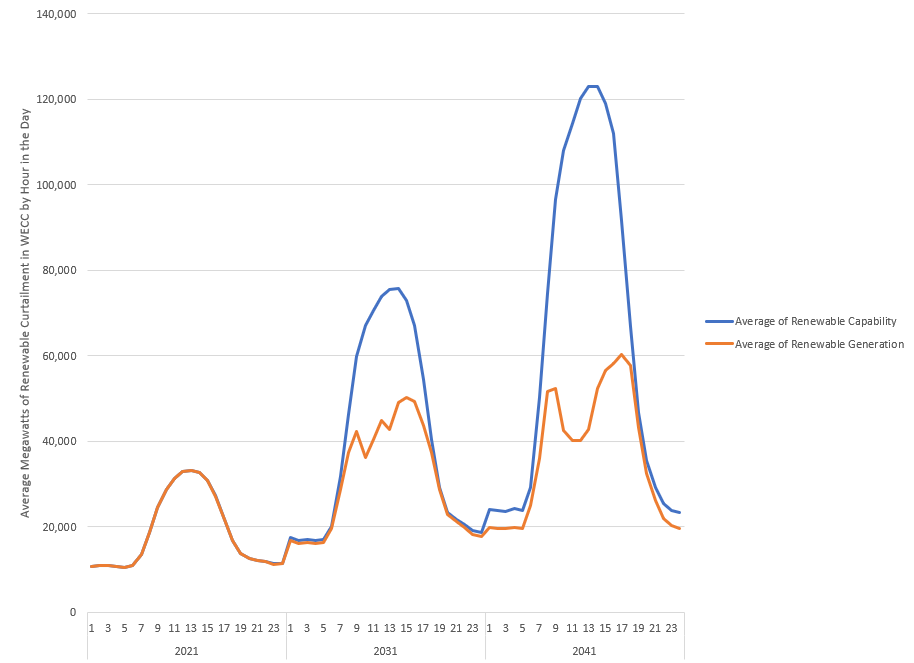

Like the baseline, but to a significantly lesser extent, a large amount of renewable generation is built, causing renewable curtailment[3] to become more prevalent throughout time, especially during midday hours. In 2021, as can be seen in the graph below, the maximum renewable generation curtailment in any hour of the day averaged just under 20 megawatts and by 2041 grew to over 81,000 megawatts. This is significantly less renewable curtailment in the limited markets study than in the baseline.

Renewable Curtailment

This extensive renewable curtailment made it challenging to enforce compliance with some of the clean policies and goals with the current technologies as can be seen in the graph below. By 2030, with current system operations,[4] transmission infrastructure and the assumed buildout the system is forecasted to not be able to meet all of obligations implied by the clean policies and goals[5] even though the buildouts contain sufficient capability to generate that much power. The state renewable portfolio standards are met for almost all years of the study.

Clean Policy Versus Capability

The following spreadsheets contain further supporting information on the limited markets scenario buildout:

Buildout Information for Limited Markets Scenario

Buildout Comparison to Baseline Conditions

Renewable Curtailment in Limited Markets Scenario

[1] The prices and market supply from this buildout are meant to simulate a picture of a less surplus market than in the baseline, but one where state policies and goals are still in effect.

[2] Since we know that planning reserve margins were not adhered to in this run, there is little incentive for the model to build for adequacy.

[3] Renewable power is often limited by how much “fuel”, insolation and wind, is available at any given time. Sometimes, more power is generated than is needed, or can be sunk to the grid due to transmission, demand or operational constraints on other generators. In this case, the power is “curtailed” or “spilled.”

[4] It is possible that revised system operations or different policy structure might reduce renewable curtailment, but the current market structure is devised to reduce production cost not to eliminate emissions.

[5] From a physical compliance inside the WECC perspective, there may be alternative compliance methods. This scenario would have to leverage heavily on these alternative measures to meet state policies and obligations.