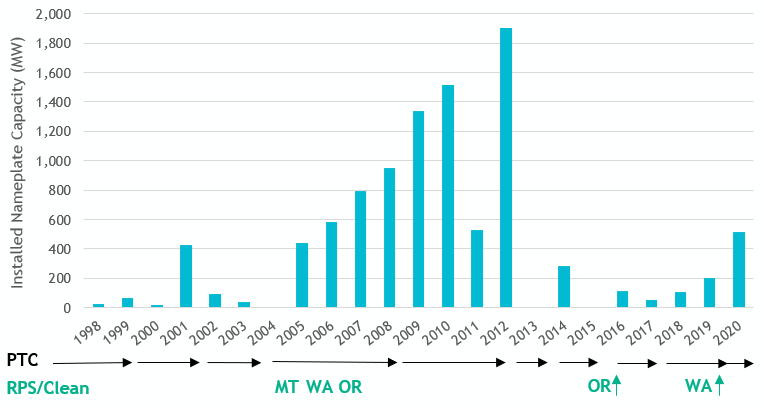

Wind

Utility-scale wind first started appearing in the region in the late 1990’s and early 2000’s. With the adoption of state renewable portfolio standards (RPS) in the mid-2000’s, wind development ramped up significantly, peaking in 2012 - a record year for wind development in the region. Uncertainty over the repeated expiration and renewal of the Production Tax Credit (PTC) and Investment Tax Credit (ITC) has led to bursts and lulls in wind development, particularly over the last decade and even more recently with the added uncertainty of Covid-19 on tax credit eligibility. (See the status of the Federal tax incentives as of Spring 2021.)

PNW Wind Development, Coincident with Federal Tax Incentives and Clean Policies

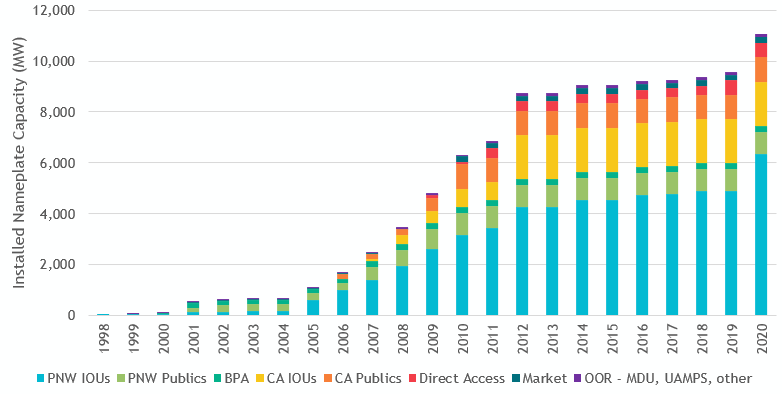

Today, the region’s wind fleet capacity is around 10,000 megawatts – although this includes some projects physically located outside the region in Wyoming and Eastern Montana that serve Pacific Northwest load (for example, some PacifiCorp and NorthWestern Energy projects). Further, about ¼ of the installed wind capacity in the region is under long-term contracts to California and other entities external to the region.

Cumulative Wind Installations, by Load

*OOR = Out of Region

Since 2012, wind development has been relatively modest. As the federal tax incentives have begun to phase down for wind, utilities and developers have been looking ahead at upcoming RPS targets, clean energy goals, and near-term energy and capacity needs and taking advantage of the credits before they expire. In addition, some of the more recent wind project developments have been spurred on by corporations directly acquiring renewable energy (without purchasing through a utility) as part of their clean energy initiatives and commitments. In order to preserve corporate customers, utilities have begun offering green power initiatives to secure renewable energy on behalf of their large customers.

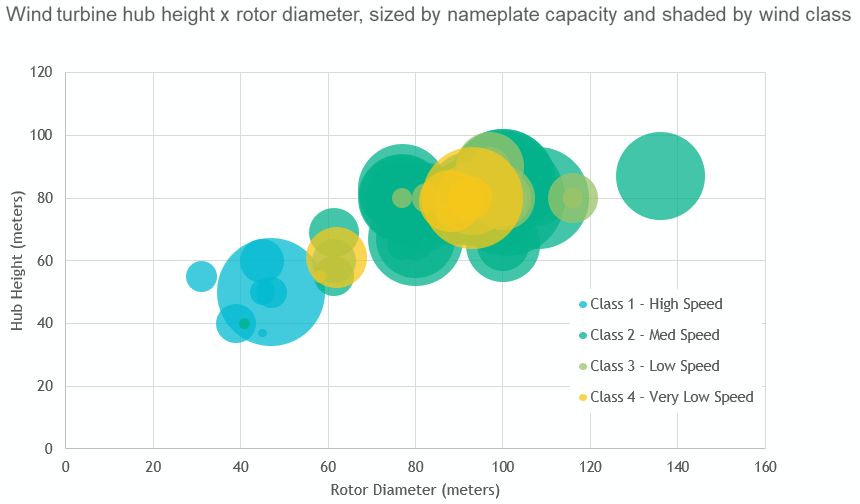

Technological advancements in wind turbine developments have aided in unlocking and reaching more wind resources than ever before. With higher hub heights and greater rotor diameters, wind turbines can access greater wind speeds at higher elevations and “sweep” more wind through the blades. These innovations have helped broaden the application and location of wind projects. Wind speeds are classified by the International Electrotechnical Commission (IEC) on a scale from 1 to 4, with class 1 being a high speed wind resource and class 4 being a very low speed wind. (These classifications are based on site wind speed, extreme gusts, and turbulence.) When wind development kicked off in the 2000’s, many of the locations were class 1 or 2 sites, to take advantage of the best wind resources available (the low hanging fruit). Now however, new developments are occurring in lower classified wind speed areas with turbines designed to maximize the wind resource available – even at low or very low wind speed classifications. In addition, advancements in the electronic components of the turbine – such as the gearbox – allow for greater control, efficiency, and reliability, and a decrease in fixed operating and maintenance costs.

Existing PNW Wind (through 2019): Hub Height x Rotor Diameter, Sized by Nameplate Capacity, Shaded by IEC Wind Class

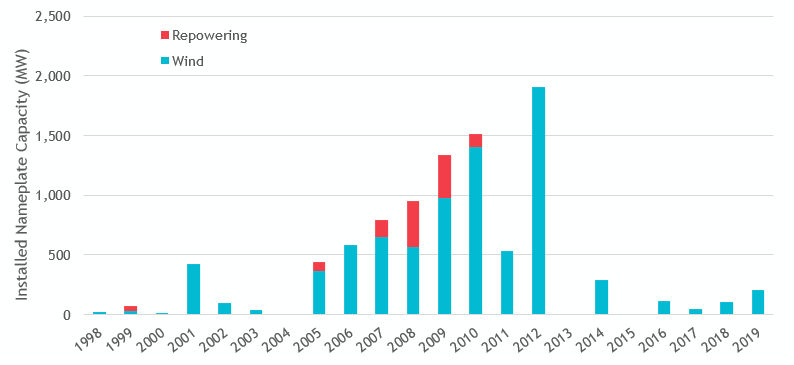

Repowering Existing Wind Projects

Repowering an existing wind project consists of replacing aging wind turbine components with new, more efficient products and technologies. For the first several generations of wind projects, the expected useful life of the wind turbines and components was about 20 years (in comparison to the more recent projects which average closer to 30 years). The average age of the existing wind fleet in the region is around 10-12 years old, although some projects are reaching the 20-year mark. As these projects age, owners can consider repowering the projects to maintain the best wind resource sites, improve the capacity and efficiency of the projects, and extend the useful life of the project. An additional incentive of repowering wind projects right now is that new turbine components qualify for federal tax incentives (PTC and ITC), which are phasing down or out at various intervals over the next few years. Due to this, some owners have chosen to repower their projects early in order to take advantage of the tax incentives before they expire, while also reaping the benefits of producing greater output at the sites and prolonging the longevity of the project through the installation of new technologies.

As of 2019, about 12% of the existing wind fleet in the region was undergoing or planned for repowering. Many of these projects were originally commissioned in the mid-to-late 2000’s, with owners hoping to capitalize on the federal tax incentives and increase the output of the projects.

Existing PNW Wind: Projects Undergoing Repowering